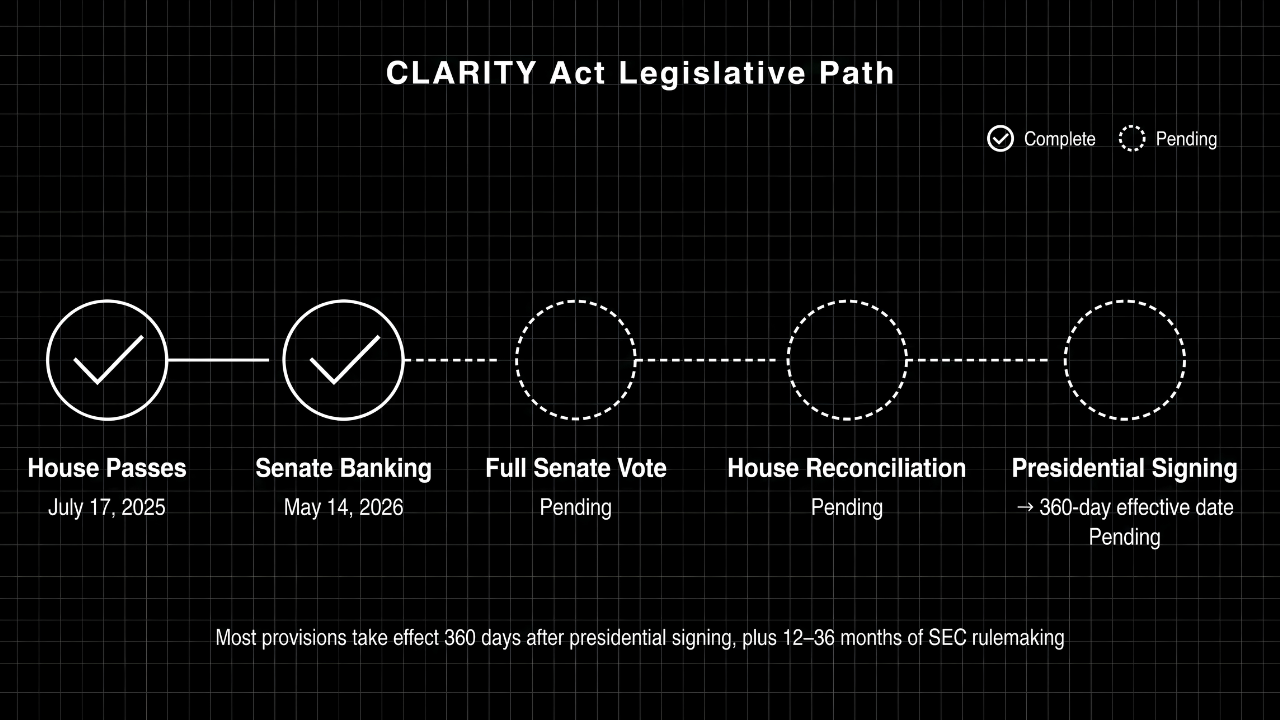

On May 14, 2026, the Senate Banking Committee passed the Digital Asset Market Clarity Act in a 15–9 vote. Two Democrats joined every Republican: Sen. Ruben Gallego of Arizona and Sen. Angela Alsobrooks of Maryland. The substitute is a Sen. Tim Scott of South Carolina product with major input from Sen. Cynthia Lummis of Wyoming and Sen. Kirsten Gillibrand of New York. It replaces the House-passed CLARITY Act text that cleared the House on July 17, 2025 by a bipartisan 294–134 vote (Roll Call No. 199). Sen. Alsobrooks signaled her floor support depends on further amendments. The bill now moves to a full Senate vote and then to reconciliation with the House version (H.R. 3633). President Trump has signaled he'll sign a final crypto market structure bill. This piece breaks down what the CLARITY Act does, what changed from the House text, and what it means for Bitcoin holders and miners.

Key Takeaways

- The Senate version is a structural rewrite of the House CLARITY Act (passed July 17, 2025, 294-134), not a minor amendment.

- Bitcoin is grandfathered as a non-security under Sec. 105(b)(2) because spot Bitcoin ETPs were listed on national exchanges before January 1, 2026.

- Self-custody is protected by federal law under Sec. 605 (the Keep Your Coins Act). Federal agencies cannot restrict it.

- Banks can custody Bitcoin, lend against Bitcoin, and provide brokerage under Sec. 401 with no new prior-approval requirement.

- Bitcoin miners get statutory cover under Sec. 601 (securities laws don't apply to validation work) and Sec. 604 (miners aren't money transmitters).

- The bill still needs full Senate passage and House reconciliation. The CFTC-side framework comes in a separate Senate Agriculture Committee bill.

What Is the CLARITY Act?

The CLARITY Act is U.S. legislation that creates a unified federal framework for cryptocurrencies and other digital assets. It splits jurisdiction between the SEC (which oversees ancillary asset issuance and securities transactions) and the CFTC (which oversees spot markets for digital commodities like Bitcoin). The Senate Banking Committee's May 14, 2026 version creates a new statutory category called a "network token" that is deemed a non-security under federal securities laws (Sec. 102, new Securities Act §4B(b)(2)).

By most accounts, the bill resolves the majority of the legal uncertainty that has shaped U.S. crypto markets since 2017. It builds on top of the GENIUS Act (already enacted in 2025) and imports the GENIUS definitions of "digital asset," "digital asset service provider," and "payment stablecoin."

The bicameral split: Banking vs. Agriculture

The Senate Banking Committee version is half of a two-committee package. The SEC-side framework, banking permissibility, software-developer protections, customer property in bankruptcy, and illicit-finance rules sit in the Banking text. The CFTC-side framework (digital commodity definitions, broker/dealer/exchange registration) is a separate Senate Agriculture Committee product. Both halves must align before the Senate sends a unified bill to conference with the House.

The new asset categories

The bill creates three primary asset categories. A network token is a digital commodity that derives its value from a distributed ledger system. It is a non-security by default. An ancillary asset is a network token whose value still depends on the efforts of a development team. Initial issuance is an investment contract; the token itself is not a security. A payment stablecoin is governed by the GENIUS Act.

What Changed From the July 2025 House Version

Rep. French Hill introduced H.R. 3633 in the House on May 29, 2025. The chamber passed it on July 17, 2025 by a bipartisan 294-134 vote (Roll Call No. 199). The bill was received in the Senate and referred to the Banking Committee on September 18, 2025 (legislative day September 16), and the Senate Banking Committee's May 14, 2026 markup is the version analyzed below.

The Senate version is a structural rewrite, not a markup. It replaces the House's "investment contract asset / digital commodity / restricted digital asset" trichotomy with a cleaner "network token / ancillary asset" dichotomy. It also adds an ETP grandfather clause that locks in Bitcoin and Ether as non-securities by statute. The House text had no comparable provision.

The most consequential differences:

| Provision | House (July 2025) | Senate (May 2026) |

|---|---|---|

| Asset framework | Investment contract asset | Network token (non-security by default) |

| Bitcoin status | Case-by-case under decentralization test | Grandfathered by statute (Sec. 105(b)(2)) |

| Self-custody | Limited protection | Federal preemption (Sec. 605, Keep Your Coins Act) |

| Banking permissibility | Narrower | 14 activities including custody, staking, lending (Sec. 401) |

| CFTC framework | Included in one bill | Deferred to Senate Agriculture |

| Anti-CBDC provisions | Included | Dropped from Senate Banking text |

| Stablecoin yield | No prohibition | Prohibited from digital asset service providers (Sec. 404) |

| Customer property in bankruptcy | Not addressed | Title VII codifies stockbroker treatment |

The Sec. 105(b)(2) grandfather clause is the single most important provision for Bitcoin holders. It says any token serving as the principal asset of a non-Investment Company Act ETP listed on a national exchange before January 1, 2026 is exempt from network token and ancillary asset treatment. Spot Bitcoin ETPs were approved by the SEC in January 2024. Bitcoin clears the bar.

Bitcoin's New Legal Status Under the CLARITY Act

Bitcoin is grandfathered as a non-security under Sec. 105(b)(2). It is the strongest statutory protection any cryptocurrency has received under U.S. law. The provision works through three connected mechanisms.

Bitcoin is a non-security by statute (Sec. 105(b)(2))

Under Sec. 105(b)(2), any token serving as the principal asset of a non-Investment Company Act ETP whose shares were listed on a national securities exchange before January 1, 2026 is exempt from network token and ancillary asset treatment. Spot Bitcoin ETPs were listed before that date. Bitcoin is grandfathered. Ether is too.

The practical effect: no certification process is needed. Bitcoin's non-security status is locked in at the statute level. The SEC cannot reverse it through rulemaking. A future administration cannot revoke it through enforcement.

Secondary market trading of Bitcoin is not a securities transaction (§4B(b)(3))

Sec. 102 adds a new Securities Act §4B(b)(3) that declares secondary market transactions in network tokens are not securities transactions. For Bitcoin, this codifies the principle established in SEC v. Ripple (2023): secondary trading is distinct from initial issuance. Buying and selling Bitcoin on an exchange, peer-to-peer, or through a derivative is protected from securities classification by statute.

The Ripple precedent is codified (Sec. 105(b)(1))

Sec. 105(b)(1) preserves any digital asset transaction found by a non-appealable final federal court judgment before enactment NOT to be a securities offering. This ratifies the 2023 SEC v. Ripple ruling and protects analogous future determinations. While most relevant to XRP, the precedent applies across the board. Programmatic secondary sales are not securities transactions.

Protections for Bitcoin Holders

Holders get three new shields: self-custody is a federal right, banks can custody and lend against Bitcoin, and customer Bitcoin gets bankruptcy protection. Each one closes a specific hole that has burned Bitcoin holders for years.

Self-custody is protected by federal law (Sec. 605)

Sec. 605 is the Keep Your Coins Act. It says no federal agency "may prohibit, restrict, or otherwise impair the ability of a covered user to self-custody digital assets using a self-hosted wallet or other means to conduct transactions for any lawful purpose."

The Bank Secrecy Act, OFAC sanctions, and anti-money-laundering enforcement powers are preserved. But the baseline right to hold your own Bitcoin in your own wallet is now federal law. Future Treasury rules cannot require KYC on every self-hosted wallet withdrawal. Future agency guidance cannot ban hardware wallets or force custody through third parties.

Banks can custody and lend against Bitcoin (Sec. 401)

Sec. 401 is the most permissive bank digital-asset framework in any major federal bill. National banks, state banks, financial holding companies, and credit unions can engage in 14 categories of digital asset activity:

- Custody of digital assets and private keys

- Staking and validator services

- Lending and lending facilitation

- Payment activities

- Principal trading

- Brokerage including clearing and execution

- Market-making

- Underwriting and dealing

- Offering self-custody wallet software

- Operating nodes and oracle services

- Digital asset derivatives

- Secondary market facilitation

- Incidental holdings

- Incidental powers

The "no other prior notice or approval requirements" language (Sec. 401(h)) replaces SAB 121 in practice by removing the prior-approval barrier. For Bitcoin holders, this means three things: bank custody options will multiply, Bitcoin-backed loans become a standard product, and Bitcoin treasury services arrive at the regional bank level. Combined with Sec. 402 (portfolio margining) and Sec. 403 (netting capital treatment), the bill creates the framework for institutional Bitcoin prime brokerage.

Bankruptcy protections for customer Bitcoin (Title VII)

Title VII amends the Bankruptcy Code's stockbroker liquidation provisions (Subchapter III of Chapter 7). Bitcoin held for customers by a digital asset broker is now treated as customer property. If a broker fails, customers get pro rata distributions from the customer property pool. They don't compete with general unsecured creditors.

This is the FTX, Celsius, and Voyager response. Customers in those cases sat for years in bankruptcy courts arguing over the basic question of whether their crypto was theirs. Title VII answers the question by statute: yes, it is.

What the CLARITY Act Means for Bitcoin Mining

Bitcoin miners get the strongest statutory protection in any federal bill to date. Sec. 601 puts validation and computational work outside the federal securities laws. Sec. 604 confirms miners are not money transmitters. Sec. 401 opens banking access for mining operations. All three protect activities that miners already perform every day on the network.

Bitcoin mining is protected as a network activity (Sec. 601)

Sec. 601 creates new Securities Act §27C and Exchange Act §15H. Both provide that a person is not subject to the federal securities laws based solely on:

- Compiling network transactions

- Relaying, searching, sequencing, or validating

- Providing computational work

- Operating a node or oracle service

- Providing network bandwidth

- Developing, publishing, or constituting distributed ledger systems and wallet software

That language describes what Bitcoin miners do every day. The protection is comprehensive: the federal securities laws "shall not apply" to these activities. The state-law preemption is sweeping. New Exchange Act §15H(g)(1) preempts every state securities, commodities, and digital asset law as applied to the protected activities. State AML, anti-fraud, and anti-manipulation laws are preserved.

The retroactive clause matters. Sec. 601(c) makes the protections apply 'before, on, or after the date of enactment.' Pending state enforcement actions premised on these activities should fall away.

Bitcoin miners are not money transmitters (Sec. 604)

Sec. 604 is the Blockchain Regulatory Certainty Act. It provides that non-controlling developers and providers:

- Are not money transmitting businesses under 31 U.S.C. §5330

- Are not engaged in money transmitting under 18 U.S.C. §1960

- Are not subject to substantially similar registration requirements

"Non-controlling" means the person does not have the legal right or unilateral ability to control, initiate, or effectuate transactions involving customer digital assets. Solo miners, mining pools that don't custody customer funds, and node operators are all inside the protection. The criminal-intent liability under 18 U.S.C. §1960(b)(1)(C) is preserved. That's the Tornado Cash and Samourai Wallet response: prosecutors retain authority to charge actors who launder criminal proceeds with intent.

For institutional miners, the read-across is direct. A 100-MW Bitcoin mining facility validating transactions on the Bitcoin network is not a money transmitter under federal law. State-level money transmitter classifications for the same activity are preempted by Sec. 601's new Exchange Act §15H(g)(1).

Banking permissibility unlocks capital access for mining

Sec. 401's banking framework changes mining operations from the capital side, not the protocol side. Three things change in the field:

- Bank lending against ASIC inventory. Banks can lend against Bitcoin mining hardware as digital asset collateral. Mining businesses get access to working capital lines that the OCC blocked under prior guidance.

- Bank custody and treasury services for Bitcoin held on balance sheet. A mining operation running its fleet under professional hosting can now use a regulated bank for custody and treasury management of mined Bitcoin.

- Banking relationships for crypto-adjacent businesses. Mining hosts, repair operations, and hardware resellers face fewer banking refusals when the activity is statutorily "financial in nature."

The bill does not change the tax treatment of mining. Mined Bitcoin is still ordinary income at fair market value on receipt, and operators still depend on bonus depreciation rules covered by the One Big Beautiful Bill Act. Tax policy and market structure policy are separate tracks.

What the CLARITY Act Does NOT Do

The bill is a market structure law, not a tax bill or an energy bill. Five honest limits matter for operators and holders:

- No change to mining tax treatment. Block rewards are still ordinary income at FMV on receipt. Bonus depreciation for ASICs comes from the One Big Beautiful Bill Act, not the CLARITY Act.

- No protection against state-level mining bans. States can still ban Bitcoin mining, impose moratoriums, set noise ordinances, or block grid interconnection. The bill preempts state securities laws for protected activities. It does not preempt state energy or zoning laws.

- No grid or environmental provisions. Nothing in the bill addresses curtailment, demand response, or emissions reporting for mining.

- No tax-policy changes for Bitcoin holders. Capital gains rules, wash sale treatment, and 1031 exchange eligibility are unchanged.

- Not yet law. The bill must clear the full Senate. It must reconcile with the House version. It needs a presidential signature. The effective date is 360 days after enactment, plus 12-36 months of SEC rulemaking.

What Happens Next

The bill has cleared the House and the Senate Banking Committee. Three steps remain before it becomes law, with an effective-date window after that.

- Full Senate floor vote. The Majority Leader sets the schedule. Sen. Alsobrooks has signaled her committee vote does not extend to the floor without further amendments. Floor amendments and a cloture path are likely. On a parallel track, the Senate Agriculture Committee's CFTC-side bill (digital commodity definitions, broker/dealer/exchange registration) must align with the Banking text before the Senate sends a unified package to conference.

- House reconciliation. Conference committee resolves differences between House and Senate versions. Key reconciliation points: the network token vs. investment contract asset framework, the Sec. 105(b)(2) ETP grandfather clause, the Anti-CBDC provisions the Senate Banking text dropped, and the stablecoin yield prohibition.

- Presidential signing. President Trump has signaled support for crypto market structure legislation.

- Effective date. Most provisions take effect 360 days after signing. SEC rulemakings on Regulation Crypto, coordinated control, and modernization add another 12-36 months.

A realistic timeline puts implementation in late 2027 or 2028. The certification regime and Reg Crypto rules will likely arrive first; the banking permissibility provisions take effect on the statutory date.

FAQs

Did the CLARITY Act pass?

Partially. The Senate Banking Committee passed it 15-9 on May 14, 2026. The House passed the original version on July 17, 2025 in a 294-134 bipartisan vote. The bill still needs a full Senate floor vote, then House reconciliation of any Senate amendments, then a presidential signature before it becomes law.

Is Bitcoin a security under the CLARITY Act?

No. Under Sec. 105(b)(2), Bitcoin is grandfathered as a non-security because spot Bitcoin ETPs were listed on national securities exchanges before January 1, 2026. The grandfather clause is permanent and cannot be reversed through SEC rulemaking.

Does the CLARITY Act protect Bitcoin self-custody?

Yes. Sec. 605 (the Keep Your Coins Act) prohibits federal agencies from prohibiting, restricting, or impairing the ability to self-custody digital assets for any lawful purpose. The Bank Secrecy Act and OFAC sanctions powers are preserved, but the right to hold your own Bitcoin in your own wallet is now federal law.

Can banks hold Bitcoin under the CLARITY Act?

Yes. Sec. 401 authorizes national banks, state banks, financial holding companies, and credit unions to custody, lend against, and provide brokerage services for Bitcoin and other digital commodities. The provision replaces SAB 121 in practice by removing the prior-approval requirements that had blocked bank custody.

How does the CLARITY Act affect Bitcoin mining?

Sec. 601 protects Bitcoin miners' validation and computational work from federal securities laws and preempts state securities laws on the same activities. Sec. 604 (the Blockchain Regulatory Certainty Act) confirms Bitcoin miners are not money transmitters. Sec. 401 banking provisions open access to capital and banking services for mining operations.

When does the CLARITY Act take effect?

If signed into law, most provisions take effect 360 days after enactment. Some provisions requiring SEC or CFTC rulemaking won't take effect until 60 days after final rule publication. The full implementation timeline runs 12-36 months after signing.

Why This Matters for Operators

Regulatory clarity does for capital what cheap power does for hashrate: it removes the variable that kept the biggest players on the sidelines. The CLARITY Act is not law yet, but it sets the floor for what the final framework will look like. Banks will custody Bitcoin. Miners will get bank credit lines. Self-custody is federal law. The operators who built infrastructure during the uncertain years now stand to scale into the cleared field.

Simple Mining is a hosted Bitcoin mining company headquartered in Cedar Falls, Iowa. We sell, host, and repair Bitcoin miners for individuals, family offices, and institutions. If you want to put capital to work in Bitcoin mining with hosting, mining hardware, and in-house repair under one roof, book a call and we'll walk you through the numbers.

This article is for educational purposes only and does not constitute legal, tax, or financial advice. The CLARITY Act has not been signed into law as of publication. Provisions, effective dates, and implementation details may change as the bill moves through the legislative process. Consult a qualified attorney or financial advisor for guidance specific to your situation.

By Josh Heine, Content Strategist at Simple Mining

Published: May 14, 2026