Bonus depreciation for Bitcoin mining is a federal tax rule that lets miners deduct 100% of qualifying ASIC and infrastructure costs in the year the equipment is placed in service, rather than spreading the deduction across MACRS's five-year recovery schedule. The One Big Beautiful Bill (OBBB) restored this treatment permanently for property placed in service after January 19, 2025, and that treatment carries into tax year 2026. Bitcoin miners running a real trade or business can deduct the full purchase price of qualifying ASICs in the year they're installed and hashing. That single deduction can wipe out mining income, slash self-employment tax, and in some cases offset W-2 wages. The catch is that "real trade or business" carries a heavy IRS test, and the rules around passive activity, material participation, and entity structure decide whether the deduction sticks.

Key Takeaways

- The One Big Beautiful Bill restored permanent 100% bonus depreciation for qualifying property placed in service after January 19, 2025, and the rule carries into tax year 2026.

- ASIC miners, supporting infrastructure (PDUs, cooling, transformers, networking), and both new and used equipment all qualify for first-year expensing when used in a Bitcoin mining trade or business.

- Bonus depreciation can only offset W-2 income when the mining activity is classified as active under Section 469, which requires meeting one of the seven material participation tests (most commonly the 500-hour or 100-hour tests).

- Entity structure changes the tax math: an S-Corp election with a reasonable W-2 salary can save roughly $1,650 in self-employment tax on a $38,000 profit and unlocks the QBI deduction.

- Documentation is the difference between a winning audit and a losing one. Dashboard screenshots, repair logs, participation calendars, and clean accounting are non-negotiable.

What Is Bonus Depreciation for Bitcoin Mining?

Bonus depreciation lets Bitcoin miners deduct 100% of the cost of qualifying ASIC hardware in the year the equipment is placed in service, rather than spreading the deduction across the IRS's standard five-year recovery schedule for mining property.

Standard depreciation under MACRS treats ASIC miners as five-year property. Without bonus depreciation, a $100,000 hardware purchase would generate roughly $20,000 in first-year deductions and the rest would unwind over four more years. Bonus depreciation collapses that schedule into year one.

Three terms matter here:

- Bonus depreciation: A first-year expensing rule that allows businesses to deduct a large percentage of qualifying asset costs in the year the property is placed in service.

- Standard MACRS depreciation: Spreads deductions across the asset's recovery period (five years for ASIC miners).

- Placed in service: The date the equipment is installed, powered on, and available for use. For hosted miners, this is the date the unit goes live in the facility and starts hashing.

Mike LaLuna, CPA at LCL Tax and a Simple Mining partner, frames it this way in his Bitcoin tax course: bonus depreciation only works when the machine is "placed in service and operating in that same tax year." A miner sitting in a warehouse on December 31 doesn't qualify. A miner installed and producing hashrate on December 31 does.

How the One Big Beautiful Bill Restores 100% Depreciation

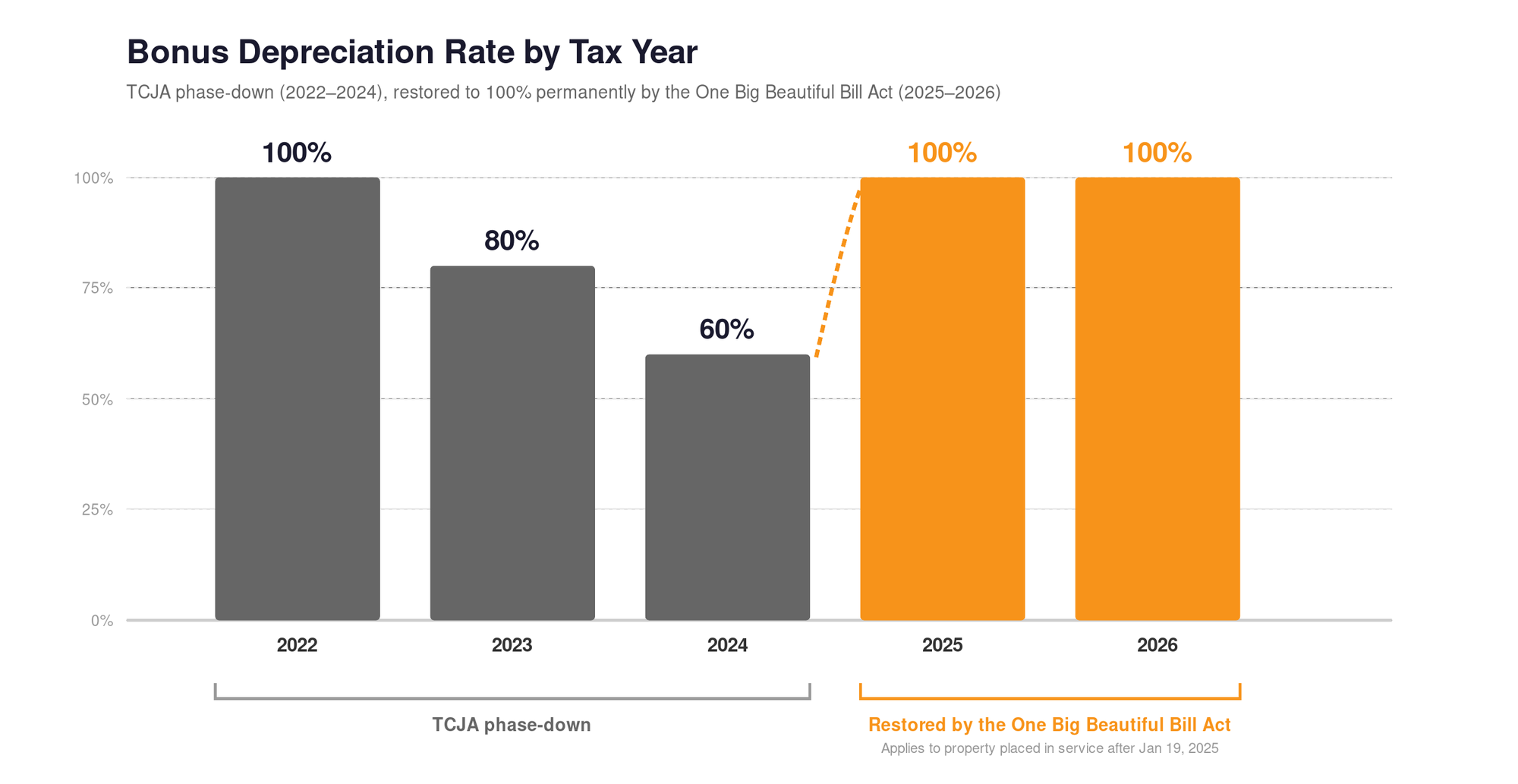

The One Big Beautiful Bill Act made 100% bonus depreciation permanent for qualifying property placed in service after January 19, 2025, reversing the phase-down that had reduced the deduction to 60% by tax year 2024.

Bonus Depreciation Phase-Down Before the Act

The 2017 Tax Cuts and Jobs Act introduced 100% bonus depreciation, then scheduled a phase-down that reduced the percentage every year. By tax year 2024 the deduction had fallen to 60%, and miners faced a shrinking window each year to capture full first-year expensing on new hardware.

What Changed for Tax Year 2026

OBBB restored permanent 100% bonus depreciation. The table below shows the rate by tax year:

| Tax Year | Bonus Depreciation Rate |

|---|---|

| 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| 2025 | 100% (restored by OBBB, retroactive to Jan 19, 2025) |

| 2026 | 100% |

For Bitcoin miners, this means a $90,000 ASIC purchase placed in service in 2026 can generate $90,000 of first-year deductions. Combined with hosting and operating expenses, a properly structured mining business can show a paper loss in year one while producing real Bitcoin income.

Bitcoin Mining Equipment That Qualifies for Bonus Depreciation

Qualifying property must have a recovery period of 20 years or less, be used in a trade or business, and be placed in service during the tax year. Most Bitcoin mining hardware fits cleanly inside these rules.

ASIC Miners and Hashrate Hardware

ASIC miners (Antminers, Whatsminers, Avalons, and equivalents) are tangible personal property with a five-year MACRS recovery period. Air-cooled units like the Antminer S21 series and hydro-cooled units like the S21 XP Hydro and S21+ Hydro both qualify. You can buy Bitcoin miners eligible for the full deduction at any time during the tax year.

Supporting Infrastructure and Components

The deduction is not limited to the miners themselves. Other qualifying items used in a mining operation include:

- Power distribution units and PDUs

- Industrial cooling systems and immersion tanks

- Electrical transformers and switchgear

- Network switches, routers, and monitoring hardware

- Server racks and containerized data center modules

Miners building out their own sites can capture significant deductions on infrastructure, not just hashrate.

New vs Used Equipment Eligibility

Both new and previously owned ASICs qualify for bonus depreciation, provided the buyer hasn't previously used the property. A refurbished S19 purchased from a marketplace or a used S21 acquired in a fleet rotation can support the same first-year deduction as a brand new unit.

Browse current Bitcoin mining hardware eligible for 2026 bonus depreciation.

Business vs Hobby Classification for Bitcoin Miners

Bonus depreciation is available only when Bitcoin mining qualifies as a trade or business, not a hobby. The IRS applies a facts-and-circumstances test focused on profit motive, time invested, and how the operation is run.

IRS Profit Motive Factors

The IRS looks at the operation as a whole. Key factors include:

- Manner of operation: Is the mining run with separate accounts, clean books, and businesslike records?

- Time and effort: Does the taxpayer (or paid staff) devote regular hours to the operation?

- Profit history and expectation: Is there a reasonable expectation of profit, even if the operation hasn't produced one yet?

- Expertise: Has the operator built knowledge of hardware, pools, hosting economics, and difficulty trends?

- Capital at risk: Is the investment sized like a business, not a casual experiment?

A miner buying ten ASICs, paying for professional hosting, tracking BTC rewards in Koinly, and monitoring a dashboard daily is operating a business. A single GPU running in a closet with no records is closer to a hobby.

Documentation That Establishes Business Intent

Mike LaLuna's tax course points to a handful of records that make the business case obvious to the IRS:

- A written business plan or investment memo

- Separate bank account (Mercury or another business-friendly bank works well)

- LLC, S-Corp, or sole proprietor filings depending on structure

- Equipment invoices and serial numbers

- Dated dashboard screenshots showing uptime and hashrate

- Mining pool statements and BTC payout records

If your records would survive a 30-minute call with an IRS examiner, you have a business. If they wouldn't, fix the records before claiming the deduction.

Section 179 vs Bonus Depreciation for Mining Hardware

Bonus depreciation usually beats Section 179 for Bitcoin miners because bonus depreciation has no income cap and can create a tax loss that offsets other income, while Section 179 cannot exceed taxable business income.

Income and Deduction Limits Under Section 179

Section 179 lets a business expense qualifying equipment in year one, but the deduction is limited to taxable business income. You cannot use Section 179 to create a net operating loss. If a mining operation generates $30,000 of net income before the deduction, Section 179 caps the write-off at $30,000 regardless of how much hardware was purchased.

When Bonus Depreciation Delivers Greater Tax Savings

Bonus depreciation has no income limitation. A $200,000 hardware purchase against $100,000 of mining income generates a $100,000 loss that flows through to the operator's personal return (subject to the material participation rules below).

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Income limitation | Yes (cannot exceed business income) | None |

| Can create a tax loss | No | Yes |

| Applies to new equipment | Yes | Yes |

| Applies to used equipment | Yes | Yes |

| Annual deduction cap | Yes | None |

| Recapture on sale | Section 1245 | Section 1245 |

Most miners default to bonus depreciation because the loss creation is where the real tax planning leverage lives.

Sole Proprietorship vs S-Corporation (Worked Example)

The entity structure changes the tax math even when the bonus depreciation deduction is identical. The math below uses the same approach Mike LaLuna walks through in his Bitcoin tax course, applied to current Simple Mining catalog pricing on the Antminer S21 XP Hydro (473 TH/s), the most popular hardware among Simple Mining clients. Revenue and operating cost figures are illustrative; actual results vary with hashprice and Bitcoin price.

- 10 Antminer S21 XP Hydro units at $9,000 each = $90,000 hardware purchase

- Illustrative mining revenue: $150,000

- Illustrative hosting and operating costs: $22,000

- Bonus depreciation: $90,000

- Pre-deduction profit: $38,000

Pricing reflects the Simple Mining catalog as of May 14, 2026. Current prices and bundle tiers available at simplemining.io/shop-miners.

As a sole proprietorship (or single-member LLC):

The $38,000 of profit is subject to self-employment tax. SE tax is calculated on 92.35% of net profit at 15.3% (12.4% Social Security up to the annual wage base limit, plus 2.9% Medicare on all earnings).

- SE tax base: $38,000 × 92.35% = $35,093

- SE tax: $35,093 × 15.3% = ~$5,369 in self-employment tax alone

- Plus ordinary income tax on the remaining profit

As an S-Corporation:

Pay yourself a reasonable W-2 salary (30% of pre-salary profit is a common starting point), then take the rest as a distribution that escapes SE tax.

- W-2 salary: $11,400

- Employer payroll tax (corporate expense): ~$872

- Net profit to S-Corp after salary and employer payroll tax: $25,728

- Owner's ordinary income tax on $25,728: ~$2,850

- Employee payroll tax withheld from salary: ~$872

- Total owner tax burden: ~$3,722

The S-Corp election saves roughly $1,650 in this scenario and unlocks the Qualified Business Income (QBI) deduction, which can knock another 20% off qualified income subject to limits.

| Tax line item | Sole Proprietorship | S-Corporation |

|---|---|---|

| Pre-deduction profit | $38,000 | $38,000 |

| W-2 salary (S-Corp only) | — | $11,400 |

| Employer payroll tax (corp expense) | — | ~$872 |

| Net flow-through profit | $38,000 | $25,728 |

| Self-employment tax | $5,369 | — |

| Ordinary income tax | varies by bracket | ~$2,850 |

| Employee payroll tax | included in SE | ~$872 |

| Total tax burden | $5,369 + income tax | ~$3,722 |

| QBI deduction available? | Yes, with limits | Yes, with limits |

The takeaway: bonus depreciation is the headline, but the entity wrapper around it determines how much of the saved tax stays in your pocket.

Passive Loss Limitations and Material Participation

Bonus depreciation only offsets your W-2 income or other ordinary income if your Bitcoin mining qualifies as an active trade or business under Section 469. If the IRS classifies your mining as passive, the bonus depreciation loss is suspended and can only offset future passive income or be released when you sell the operation.

This is the single most important section of this guide. Most articles gloss over passive activity rules. The miners who get burned aren't the ones who picked the wrong hardware. They're the ones who claimed a six-figure deduction against W-2 income and then failed the material participation test on audit.

How Section 469 Restricts Mining Deductions

Under Section 469, net losses from a passive activity can only offset income from another passive activity. Passive losses cannot offset wages, salary, portfolio income, or income from active businesses you operate. Suspended passive losses carry forward until you generate passive income or dispose of the activity.

Real estate investors have carve-outs like Real Estate Professional Status and the $25,000 "mom and pop" exception. Bitcoin miners have none of those. The only path to active treatment is material participation.

Seven Tests for Material Participation

The IRS has seven material participation tests. You only need to meet one. All seven:

- The 500-hour test. You participate in the mining activity for more than 500 hours during the tax year.

- The substantially-all test. Your participation makes up substantially all of the participation in the activity by anyone (including non-owners).

- The 100-hour test. You participate for more than 100 hours and no other individual participates more than you do.

- Significant participation aggregate test. Aggregate participation over 500 hours across multiple significant-participation activities.

- 5-of-10 test. Material participation in five of the prior ten tax years.

- Personal service activity test. Participation in three prior years for personal service activities.

- Facts and circumstances test. Regular, continuous, and substantial involvement based on overall facts.

The 500-hour test and the 100-hour test are the cleanest paths for most Bitcoin miners. The 100-hour test is realistic for hosted operators who don't physically touch hardware but make all operational decisions.

What Hosted Miners Need to Document

Hosted mining does not automatically make you passive. Material participation is determined by the shareholder's involvement, not the entity type or whether someone else racks the hardware. A miner who uses professional hosting but personally selects hardware, monitors uptime, manages pool routing, and makes capital decisions can support an active classification.

What we see work in practice:

- Logs and calendars. Time spent reviewing the dashboard, reading market analysis, evaluating new hardware, communicating with the host.

- Dated screenshots. Weekly captures of the Simple Mining dashboard showing hashrate, uptime, and earnings.

- Decision documentation. Emails, memos, or notes covering pool selection, curtailment decisions, repair authorizations, and upgrade plans.

- Repair tickets. Records of conversations with the in-house repair facility when units need service.

- Communication trails. Regular contact with your hosting team. Simple Mining's overcommunication standard means clients receive proactive curtailment and uptime updates that double as participation evidence.

Bottom line: bonus depreciation only offsets your W-2 income if your mining qualifies as active. Hosted mining can qualify, but only if you can document material participation. The dashboard and client engagement model at Simple Mining supports that documentation. It does not guarantee the classification.

For miners pursuing this strategy, the right move is to consult a CPA who handles mining returns. Mike LaLuna's firm at lcltax.com/bitcoin-mining-bookkeeping-plans specializes in exactly this question.

See how Simple Mining's hosted mining facility and client dashboard can support your material participation documentation.

How Bitcoin Mining Compares to Real Estate Depreciation

Bitcoin mining and real estate are the two main asset classes Americans use to convert capital into depreciation deductions. Mining offers faster first-year expensing and higher returns. Real estate offers longer asset lives and (in some cases) easier passive activity carve-outs.

Returns and Scalability

A solid commercial real estate investment nets 8–12% annually. A well-structured Bitcoin mining operation can produce higher annual returns when hashprice and power costs are favorable, with some operators reporting 20–40%+ in strong Bitcoin price environments. Returns vary significantly with Bitcoin price, network difficulty, and hosting rates. Scaling mining means buying more ASICs and adding hosting slots. Scaling real estate means hunting for new properties, closing on them, and managing tenants.

Liquidity and Exit Flexibility

ASIC miners can be sold within days through a marketplace or peer transaction. Real estate sales take months and involve agents, inspections, financing contingencies, and closing costs. Mining hardware can also be relocated. A property cannot.

Operating Costs and Management Complexity

Hosted mining at Simple Mining bundles power, monitoring, and maintenance into a single hosting fee. Real estate carries property taxes, insurance, repairs, vacancies, tenant management, and unpredictable capital expenditures. The operational surface area is smaller with mining.

The trade-off: real estate has 27.5- or 39-year depreciation schedules that produce slow, predictable shelter. Mining concentrates the deduction in year one. Different strategies for different planning horizons.

Additional Tax Deductions for Bitcoin Mining Operations

Beyond the depreciation deduction on hardware, ongoing mining operations generate deductible expenses every month. These reduce taxable mining income further.

Hosting Fees

Monthly hosting fees paid to a colocation provider are fully deductible as ordinary business expenses. Hosted customers pay a single all-in rate that covers power, infrastructure, monitoring, and site operations. The full amount is deductible.

Repairs and Maintenance Expenses

Repair costs on Bitcoin miners are deductible. For miners purchased through Simple Mining, the first 12 months of repairs are covered under the Miner Protection program at no additional cost. After that window, repairs run through the in-house repair facility at standard rates. Parts, labor, and shipping for any uncovered repair are all deductible.

Other Deductible Operating Costs

A complete list of common deductions for a Bitcoin mining business:

- Hosting fees

- Repairs, replacement parts, and shipping

- Mining pool fees (Luxor, NiceHash, Ocean, etc.)

- Internet and networking costs at any owned sites

- Professional services (CPA, attorney, bookkeeper)

- Business banking fees

- Software subscriptions (Koinly, accounting tools)

- Conference travel directly tied to the mining business

Track each line item monthly. The combination of bonus depreciation plus operating expenses is what produces meaningful net losses in year one.

Documentation Requirements for Mining Depreciation Claims

The IRS expects contemporaneous records that support every claimed deduction. Reconstructed records weaken your position in an audit. Real-time tracking strengthens it.

Essential Records for Audit Protection

Maintain at minimum:

- Purchase invoices showing the date, amount, and serial numbers of each unit

- Proof of payment (bank transfers, ACH receipts, wire confirmations)

- Placed-in-service documentation (installation date, first hashrate reported)

- Business use records (dashboard screenshots, uptime logs, pool payouts)

- Income and expense logs tied to the operation's bank account

- Material participation logs if you're claiming active treatment

How Mining Dashboards Support Compliance

A professional hosting dashboard creates a contemporaneous business record automatically. Simple Mining's dashboard logs hashrate, uptime percentage, billing line items, and pool earnings in real time. The Repair Report Dashboard logs every service event. Both are downloadable, dated, and tied to the specific machines in your account. That kind of audit trail is exactly what the IRS wants to see when it asks how you knew your equipment was placed in service on a specific date and operating throughout the year.

Depreciation Recapture When Selling Mining Equipment

When you sell a previously depreciated ASIC, the IRS recaptures the depreciation as ordinary income up to the amount of depreciation previously claimed. Any gain above the original purchase price is treated as capital gain.

Example: You bought an Antminer S21 XP Hydro for $9,000 and claimed $9,000 of bonus depreciation in year one. Two years later you sell the unit for $4,500. Your adjusted basis is $0 (fully depreciated), so the entire $4,500 sale price is depreciation recapture taxed at ordinary income rates under Section 1245. Unlike real estate, which gets a 25% cap on unrecaptured Section 1250 gain, personal property recapture is taxed at your full marginal rate, which can reach 37%.

Plan for this at exit. If you intend to sell a fleet during a strong hardware market, the recapture can be significant. Strategies to manage it include staggering sales across tax years, reinvesting proceeds in new hardware (which generates fresh bonus depreciation to offset the recapture), and considering a 1031-style strategy in some structures (consult your CPA: most personal property no longer qualifies for like-kind exchange treatment post-TCJA).

Recapture applies to the mining hardware. The Bitcoin you mined is taxed separately under Bitcoin capital gains rules when you sell it, and if any of those holdings are underwater you can harvest the losses to offset your gains.

FAQs

Can I claim bonus depreciation if my Bitcoin miners are hosted by a third party?

Yes. Ownership of the hardware and qualification as a trade or business are what matter. A hosting provider operating the machines on your behalf does not disqualify the deduction. Material participation is still required if you want to offset W-2 income.

Does bonus depreciation apply to used or refurbished ASIC miners?

Yes. Both new and previously owned mining equipment qualify, as long as you (the buyer) haven't previously used the property and it's used in your trade or business. A refurbished S19 placed in service in 2026 supports the same first-year deduction as a new unit.

How do state taxes treat Bitcoin mining depreciation deductions?

State treatment varies. Some states conform to federal bonus depreciation. Others require multi-year depreciation regardless of federal rules. California does not conform to federal bonus depreciation and requires separate depreciation calculations. Pennsylvania, New Jersey, and several other states maintain their own rules. Iowa's conformity status has shifted over time. Confirm with a CPA familiar with your state.

What happens to my depreciation deduction if I pause my Bitcoin mining operation?

A pause does not automatically disqualify prior depreciation claims. Extended inactivity (multiple years with no hashing, no income, no operational decisions) can raise hobby reclassification questions on audit. Document the reason for the pause and the date you intend to resume.

Can I claim bonus depreciation on Bitcoin miners purchased late in the tax year?

Yes. Equipment placed in service at any point during the tax year qualifies for full 100% bonus depreciation. A unit installed and hashing on December 30, 2026 produces the same deduction as one installed on January 2, 2026. The placed-in-service date is what matters, not the number of operational days in the year.

Run the Tax Math Before You Buy

Bonus depreciation rewards miners who treat their operation like a business. The deduction is generous, the rules are clear, and the audit risk is manageable when the records are clean.

Disclaimer: This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual situations vary. Consult a qualified CPA or tax professional before making decisions based on this information. Simple Mining partners with Mike LaLuna, CPA at LCL Tax, who specializes in Bitcoin mining taxation and can be reached at lcltax.com. State tax treatment of bonus depreciation varies. Some states conform to federal rules. Others require multi-year depreciation. Confirm with your state's tax authority or a CPA familiar with your state.

The miners who capture the most value combine three things: the right hardware, hosted operations that support material participation, and a CPA who handles mining returns every year. Simple Mining provides the first two. Mike LaLuna's firm provides the third.

Schedule a call with our team to discuss equipment, hosting, and how Mike LaLuna's tax expertise integrates with your mining setup.

By Josh Heine, Content Strategist at Simple Mining

Published: July 19, 2024

Modified: June 24, 2026